{kind=link}

Freelancing has grow to be one of the vital fashionable profession decisions in India. Writers, designers, builders, consultants, and entrepreneurs are all constructing impartial careers and incomes stable incomes with no conventional employer. However with that freedom comes a accountability freelancers would possibly overlook: paying tax appropriately. Understanding freelancer revenue tax in India just isn’t non-obligatory. It’s a authorized requirement, and getting it improper can result in penalties, curiosity expenses, and undesirable consideration from the tax division.

This information breaks down every thing a freelancer in India must learn about submitting revenue tax in 2026.

Why Freelancer Revenue Tax in India Works In a different way

Whenever you work for a corporation as an worker, your employer deducts tax at supply and arms you a Type 16 on the finish of the yr. As a freelancer, there isn’t any employer doing this for you. Your revenue is handled as “revenue from enterprise or occupation,” not wage. This single distinction modifications every thing about the way you calculate, report, and pay tax.

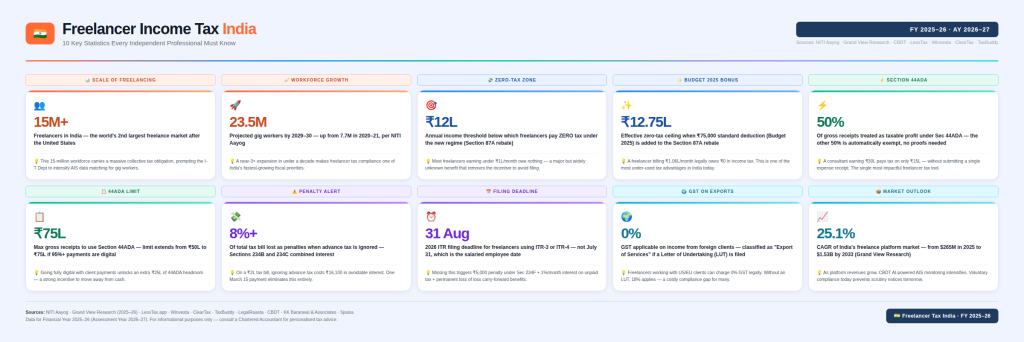

Freelancer revenue tax in India applies the second your complete revenue for the monetary yr crosses the fundamental exemption restrict. It doesn’t matter whether or not your shoppers are in Mumbai or in New York. In case you are a tax resident of India, your worldwide freelance revenue is taxable right here, together with funds obtained via freelance platforms.

Step 1: Know Your Revenue Tax Slabs for FY 2025-26

The largest replace affecting freelancer revenue tax in India this yr is the brand new tax regime. It stays the default system for all taxpayers, together with these incomes via enterprise or occupation, underneath Part 115BAC. The Union Funds 2026 made no modifications to those slabs, so the charges that utilized for FY 2025-26 proceed into FY 2026-27 as effectively.

New Tax Regime slabs (FY 2025-26, AY 2026-27):

| Revenue Vary | Tax Charge |

| As much as ₹4 lakh | Nil |

| ₹4 lakh to ₹8 lakh | 5% |

| ₹8 lakh to ₹12 lakh | 10% |

| ₹12 lakh to ₹16 lakh | 15% |

| ₹16 lakh to ₹20 lakh | 20% |

| ₹20 lakh to ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

Because of the Part 87A rebate, revenue as much as ₹4 lakh is tax-free, and the best charge of 30% solely applies above ₹24 lakh. This rebate successfully means freelancers with taxable revenue as much as ₹12 lakh underneath the brand new regime can find yourself paying zero tax, which is a significant aid for early-career freelancers and small consultants.

Outdated Tax Regime:

This selection nonetheless exists when you favor to assert deductions like 80C investments, 80D medical health insurance premiums, and residential mortgage curiosity. Underneath the previous regime, revenue as much as ₹2.5 lakh is tax-free, and tax begins at 5% between ₹2.5 lakh and ₹5 lakh, rising via the same old slabs to 30% for revenue above ₹10 lakh. If in case you have heavy investments or deductions to assert, the previous regime would possibly nonetheless work out cheaper, so it’s price evaluating each earlier than submitting.

Step 2: Select How You Wish to Calculate Your Revenue

As a freelancer, tax doesn’t apply to every thing you earn. It applies to your revenue, which is your complete receipts minus the cash you spend to do your work. The federal government offers you two methods to calculate this revenue. Which methodology works for you is dependent upon your occupation, your annual earnings, and the way excessive your actual bills are.

Possibility A: Presumptive Taxation underneath Part 44ADA

Part 44ADA lets specified professionals declare 50% of their gross receipts as taxable revenue, no matter what they really spent on bills. This implies:

- You do not want to keep up detailed books of accounts.

- You do not want a tax audit, even when your revenue is substantial.

- You pay tax on half your earnings and transfer on.

Eligibility for Part 44ADA:

- You should be in a specified occupation, resembling authorized, medical, engineering, structure, accountancy, technical consultancy, inside ornament, or related skilled and inventive freelance work.

- Your annual gross receipts should not exceed ₹50 lakh, or ₹75 lakh if lower than 5% of your complete receipts are in money.

- You need to declare at the least 50% of receipts as revenue. Declaring decrease and nonetheless utilizing this scheme just isn’t permitted.

Contemplate an instance: Ravi is a contract inside decorator incomes ₹30 lakh in receipts in the course of the yr. His precise bills, together with lease, telephone payments, and journey, come to ₹10 lakh. As an alternative of calculating his actual revenue, Ravi opts for Part 44ADA and declares ₹15 lakh (50% of ₹30 lakh) as his taxable revenue. This protects him from sustaining detailed books and simplifies his return significantly.

Possibility B: Submitting Revenue Tax on Precise Earnings (ITR-3)

In case your precise bills exceed 50% of your receipts, or in case your gross receipts cross the ₹75 lakh restrict, it’s essential to transfer to the common methodology. Right here, you calculate your actual revenue by subtracting real enterprise bills out of your gross receipts. These can embody software program subscriptions, web payments, a portion of lease for a house workplace, and advertising prices. This route requires sustaining correct books of accounts, and in case your receipts exceed sure thresholds, a tax audit turns into obligatory.

Contemplate an instance: Priya is a software program developer with ₹80 lakh in gross receipts, break up between ₹40 lakh from international shoppers on Upwork and ₹40 lakh from Indian shoppers. Her actual bills complete ₹45 lakh, masking software program instruments, a house workplace, web, advertising, journey, and accounting charges. As a result of her receipts exceed the ₹75 lakh presumptive restrict, Priya should file underneath ITR-3, preserve correct books, and get her accounts audited.

Step 3: Dealing with International Consumer Revenue

A rising share of Indian freelancers work with worldwide shoppers, and freelancer revenue tax in India applies totally to this revenue too, since Indian residents are taxed on their international earnings. To deal with it appropriately:

- Convert to INR: Use the financial institution’s change charge on the date the fee lands in your account, and report the complete quantity earlier than any platform deducts its service charges.

- Choose your calculation methodology: Apply Part 44ADA when you qualify, or calculate precise revenue and file ITR-3 in case your receipts are increased or bills exceed 50%.

- Apply the tax slabs: Use both the brand new or previous regime charges in your closing taxable revenue, after subtracting any eligible deductions.

- Declare aid for international tax already paid: If a international shopper’s nation deducted tax, for instance the US deducting 30% on sure funds, you may declare that quantity again as a credit score utilizing Type 67. India’s Double Taxation Avoidance Agreements with numerous international locations exist particularly to stop the identical revenue from being taxed twice.

Step 4: Understanding TDS

Many Indian shoppers are legally required to deduct tax earlier than paying you. TDS, known as Tax Deducted at Supply, underneath Part 194J applies at 10% for skilled and technical companies.

This isn’t an extra tax. Consider it as tax paid early in your behalf. Whenever you file your return on the finish of the yr, you declare full credit score for no matter your shoppers deducted, and the tax authority adjusts it in opposition to your complete tax legal responsibility.

One necessary behavior to construct: at all times examine your Type 26AS and Annual Info Assertion on the revenue tax portal earlier than submitting. These paperwork present precisely how a lot TDS the federal government has on document for you. If the figures don’t match what your shoppers truly deducted, it might probably set off a tax discover. Catching mismatches early saves quite a lot of hassle later.

Step 5: Pay Advance Tax on Time

In case your tax legal responsibility exceeds ₹10,000, it’s essential to pay advance tax somewhat than settling all of it at year-end. Salaried workers hardly ever take care of this as a result of their employer handles most of it via TDS. For freelancers, TDS from shoppers could cowl a part of your legal responsibility, but it surely hardly ever covers all of it, particularly if in case you have a number of revenue sources or your earnings develop via the yr. You have to pay the remaining tax upfront. Lacking it results in curiosity expenses underneath Sections 234B and 234C.

- In case you go for Part 44ADA and don’t have any different main revenue supply, you may pay 100% of your advance tax in a single installment on or earlier than 15 March of the monetary yr.

- In case you file underneath common provisions (ITR-3) or produce other revenue like wage, lease, or capital beneficial properties alongside your freelance work, it’s essential to comply with the usual four-installment schedule, with funds due in June, September, December, and March.

Late or underpaying triggers computerized curiosity. Estimate your annual revenue early and set funds apart quarterly, not scrambling in March.

Step 6: File the Appropriate ITR Type

Selecting the best kind issues as a lot as calculating the appropriate tax.

- ITR-4 (Sugam): Use this in case you are choosing presumptive taxation underneath Part 44ADA and don’t have any issues like capital beneficial properties or international property.

- ITR-3: Use this in case you are calculating precise income, have capital beneficial properties, personal multiple home property, have international revenue or property, or don’t qualify for the presumptive scheme.

The submitting course of usually entails logging into the revenue tax e-filing portal, checking your AIS and TIS to substantiate what revenue the division already has on document, filling in what you are promoting or skilled revenue particulars, submitting Type 10-IEA in case you are switching between the previous and new regimes, and finishing Aadhaar OTP verification to make your submitting legitimate.

Do You Want a Tax Advisor?

Freelancer revenue tax in India entails a number of transferring components: selecting the best regime, choosing between presumptive and precise taxation, monitoring TDS, managing advance tax deadlines, and dealing with international revenue guidelines. For a lot of freelancers, particularly these simply beginning out with a single revenue supply and easy earnings, submitting independently is fully manageable when you perceive the fundamentals.

Nevertheless, a small mistake, like lacking an advance tax installment, submitting the improper ITR kind, or misreporting international revenue, can result in penalties that price greater than skilled assist would have. That is the place a tax advisor turns into beneficial.

An excellent tax advisor does extra than simply file your return. They allow you to determine between the previous and new regime based mostly in your precise numbers, advise on whether or not Part 44ADA genuinely advantages you, and ensure your TDS credit and international revenue are reported appropriately. For freelancers juggling a number of shoppers, worldwide funds, or rising revenue, dependable tax consulting companies liberate time and considerably cut back the danger of expensive errors.

In case your revenue is rising, your shopper base is increasing internationally, or you’re merely uncertain about any step within the course of, investing in tax consulting companies is a sensible determination somewhat than an pointless expense.

Often Requested Questions (FAQs)

Q1. Do freelancers must pay revenue tax in India?

Sure. Any freelancer incomes above the fundamental exemption restrict is required to pay revenue tax in India. Freelance revenue is handled as revenue from enterprise or occupation, which suggests the identical tax slabs and submitting guidelines apply. New tax regime: ₹4 lakh exemption restrict, zero tax as much as ₹12 lakh with Part 87A rebate.

Q2. Which ITR kind ought to a freelancer file?

Freelancers choosing presumptive taxation underneath Part 44ADA ought to file ITR-4. These calculating precise income, incomes from international shoppers, or having capital beneficial properties alongside freelance revenue ought to file ITR-3. Submitting the improper kind is a typical mistake and may result in a faulty return discover from the tax division.

Q3. What’s Part 44ADA and who can use it?

Part 44ADA is a presumptive taxation scheme that enables specified professionals to declare 50% of their gross receipts as taxable revenue, with out sustaining detailed books of accounts. It’s obtainable to freelancers in fields like engineering, authorized, medical, structure, technical consultancy, and inside ornament, supplied their annual gross receipts don’t exceed ₹50 lakh, or ₹75 lakh if lower than 5% of receipts are in money.

This autumn. Is freelance revenue from international shoppers taxable in India?

Sure. In case you are a tax resident of India, your revenue from international shoppers is totally taxable right here no matter which nation the shopper relies in or which platform you used to obtain fee. You need to convert the quantity to INR utilizing your financial institution’s change charge on the date of receipt and report the complete quantity earlier than any platform deductions. If tax was already deducted within the international nation, you may declare aid underneath India’s Double Taxation Avoidance Agreements utilizing Type 67.

Disclaimer: This text is meant for informational functions solely and doesn’t represent tax recommendation. Tax legal guidelines and deadlines are topic to vary. Please seek the advice of a professional tax advisor earlier than making any submitting choices.