{kind=link}

[Rewritten on July 7, 2025 after the new 2025 Trump tax law was passed.]

As a result of I’m self-employed and I’m below 65, I purchase medical health insurance from the medical health insurance market established below the Reasonably priced Care Act (ACA). Each state has one. Some states run their very own. Some states use the federal healthcare.gov platform. It’s for the self-employed, early retirees, and others who don’t get medical health insurance by an employer or a authorities program resembling Medicaid or Medicare.

You qualify for a Premium Tax Credit score (PTC) once you purchase medical health insurance from the ACA market primarily based in your modified adjusted gross revenue (MAGI) relative to the Federal Poverty Degree (FPL) on your family dimension. Generally, the decrease your MAGI is, the much less you pay for medical health insurance internet of the tax credit score.

MAGI for ACA

Your MAGI for ACA is principally:

- Your gross revenue

- plus tax-exempt muni bond curiosity

- plus untaxed Social Safety advantages

- minus pre-tax deductions from paychecks (401k, FSA, HSA, …)

- minus above-the-line deductions listed on web page 2 of Kind 1040 Schedule 1, for instance:

- pre-tax conventional IRA contributions

- HSA contributions made outdoors of payroll

- 1/2 of self-employment tax

- pre-tax contributions to SEP-IRA, solo 401k, or different retirement plans

- self-employed medical health insurance deduction

- scholar mortgage curiosity deduction

Wages, 1099 revenue, rental revenue, curiosity, dividends, capital positive factors, pension, withdrawals from pre-tax conventional 401k and IRAs, and Roth conversions all go into the MAGI for ACA. Muni bond curiosity and untaxed Social Safety advantages additionally depend within the MAGI for ACA.

Tax-free withdrawals from Roth accounts don’t enhance your MAGI for ACA.

Facet be aware: There are a lot of totally different definitions of MAGI for various functions. These totally different MAGIs embrace and exclude totally different elements. We’re solely speaking in regards to the MAGI for ACA right here.

2021-2025: 400% FPL Cliff Modified to a Slope

Your premium tax credit score goes down as your MAGI will increase. Up by the 12 months 2020, the tax credit score dropped to zero when your MAGI went above 400% of the Federal Poverty Degree (FPL). In case your MAGI was $1 above 400% of FPL, you’d pay the complete premium on your ACA medical health insurance with zero tax credit score.

Legal guidelines modified throughout COVID. This 400% FPL cliff turned a downward slope for 5 years, from 2021 to 2025. The tax credit score continued to drop as your MAGI elevated, but it surely didn’t all of the sudden drop to zero in case your revenue went $1 over 400% of FPL. The tax credit score at revenue ranges beneath 400% of FPL additionally turned extra beneficiant throughout these 5 years.

The Cliff Returns in 2026

The brand new 2025 Trump tax legislation — One Large Stunning Invoice Act — didn’t prolong the improved tax credit score after 2025. The 400% FPL cliff is scheduled to return in 2026. The premium tax credit score at incomes beneath 400% of FPL will even drop again to pre-COVID ranges.

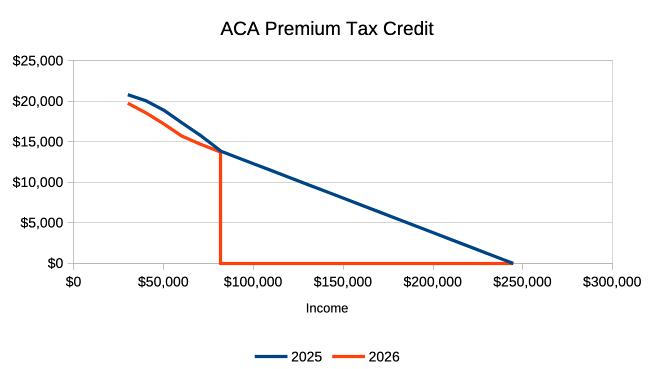

The chart above illustrates the ACA premium tax credit score at numerous revenue ranges for a pattern family of two 55-year-olds residing within the decrease 48 states. The blue line is for 2025, with the slope and the improved tax credit score. The pink line is for 2026, with out the improved tax credit score. The sharp vertical drop is the cliff.

Variable Influence

How your premium tax credit score will change in 2026 relies on your place within the chart.

In case your MAGI is to the left of the cliff within the chart, your tax credit score will drop barely. It goes down from $18,900 to $17,200 at a $50,000 revenue on this instance. A $1,700 drop within the tax credit score interprets to a rise of about $140/month for medical health insurance. Having a $140/month enhance isn’t nice, however maybe it’s manageable when you’re ready.

Your tax credit score will drop extra in case your revenue is to the far proper within the chart. At a $200,000 revenue on this instance, the tax credit score drops from $3,800 to $0, elevating the price for medical health insurance by somewhat over $300/month. Nobody needs a giant hit to their funds, however a minimum of you’ve the revenue to afford it.

The drop is precipitous instantly to the proper of the cliff. We’re speaking about receiving a $13,000 tax credit score in 2025 versus $0 in 2026 at an revenue of $85k. How do you provide you with an additional $13,000 for medical health insurance when your revenue is $85k?

I used information from KFF’s premium subsidy calculator for my instance. You’ll be able to enter your particular zip code, family dimension, and age on this calculator to estimate how a lot your premium tax credit score and your internet medical health insurance premium will change.

Know Your Cliff

You need to know at the beginning the place the cliff is for you. The desk beneath reveals the 400% FPL cliff for numerous family sizes in 2026:

| Family Dimension | Decrease 48 States | Alaska | Hawaii |

|---|---|---|---|

| 1 | $62,600 | $78,200 | $71,960 |

| 2 | $84,600 | $105,720 | $97,280 |

| 3 | $106,600 | $133,240 | $122,600 |

| 4 | $128,600 | $160,760 | $147,920 |

| 5 | $150,600 | $188,280 | $173,240 |

| 6 | $172,600 | $215,800 | $198,560 |

| 7 | $194,600 | $243,320 | $223,880 |

| 8 | $216,600 | $270,840 | $249,200 |

Supply: Federal Poverty Ranges (FPL) For Reasonably priced Care Act.

The chart I used for example is for a two-person family. A chart on your particular state of affairs can have the identical form however totally different numbers on the axes.

In case your MAGI is safely to the left of the cliff and there’s no threat of going over, be ready for a rise in your medical health insurance premiums in 2026 because of the slight lower within the premium tax credit score. If it’s far to the left, look ahead to a unique cliff on the low finish, which I’ll clarify on the finish of this publish.

In case your MAGI is just too far to the proper of the cliff and you’ve got completely no method to carry it to the left, you’ll should pay 100% of the medical health insurance premium beginning in 2026, which may be properly over $20,000 a 12 months.

The difficult half and the alternatives are within the center. In case your MAGI is near the cliff on either side, it is best to handle it rigorously to maintain it from going over the cliff.

Handle Your Revenue

Essentially the most essential half is to venture your MAGI all year long and to not notice revenue willy-nilly. You’ll be able to nonetheless alter when you discover your revenue is about to go over the cliff earlier than you notice revenue. Many individuals are caught unexpectedly solely once they do their taxes the next 12 months. Your choices are way more restricted after the 12 months is over.

If revenue from working will push your MAGI over the cliff, possibly work rather less to maintain it below.

Tax-free withdrawals from Roth accounts don’t depend as revenue.

Check out the MAGI definition. Reduce objects that increase your MAGI, and maximize all the pieces that lowers your MAGI.

When you’ve W-2 or self-employment revenue, you’ve the choice to contribute to a pre-tax conventional 401k and IRA. These pre-tax contributions decrease your MAGI, which helps you keep below the 400% FPL cliff.

Select a high-deductible plan and contribute the utmost to an HSA. The brand new 2025 Trump tax legislation made all Bronze plans from the ACA market HSA-eligible beginning in 2026.

Then again, Roth conversions, withdrawals from pre-tax accounts, and realizing capital positive factors enhance your MAGI. You need to be cautious with doing these once you’re making an attempt to remain below the 400% FPL cliff.

Shifting Revenue

For those who’re liable to going over the cliff in 2026, contemplate accelerating some revenue from 2026 to 2025 when the premium tax credit score remains to be on a slope. If pulling revenue ahead to 2025 helps you keep below the cliff in 2026, you lose a lot much less in premium tax credit score out of your extra revenue in 2025 than the steep drop in 2026.

Then again, when you’re going over the cliff in 2026 it doesn’t matter what, contemplate suspending some revenue from 2025 to 2026. When you’re over the cliff in 2026, you don’t have anything extra to lose, whereas much less revenue provides you with extra premium tax credit score in 2025.

Borrowing

You probably have a short lived spike in your want for extra cash, contemplate borrowing as a substitute of withdrawing from pre-tax accounts or realizing massive capital positive factors. Spending borrowed cash doesn’t depend as revenue.

If you want money to purchase a brand new automotive, as a substitute of realizing massive capital positive factors and pushing your self over the cliff, take a low-APR automotive mortgage to stretch it out. HELOC, security-based lending, and promoting brief field spreads are additionally good sources for borrowing.

You’ll be able to repay the mortgage once you don’t want as a lot money or once you not use ACA medical health insurance.

Revenue Bunching

For those who can’t keep away from going over the 400% FPL cliff, contemplate revenue bunching. If you’re already over the cliff, you may as properly go over huge. Withdraw extra from pre-tax accounts or notice extra capital positive factors and financial institution the cash for future years.

Spending the banked cash doesn’t depend as revenue. Going over the cliff huge time in a single 12 months could make it easier to keep away from going over once more for the following a number of years.

100% and 138% FPL Cliff

There’s one other cliff on the low finish, though that one is definitely overcome you probably have pre-tax retirement accounts.

To qualify for a premium tax credit score for getting medical health insurance from the ACA market, your MAGI have to be above 100% of FPL. In states that expanded Medicaid, your MAGI have to be above 138% of FPL. This map from KFF reveals which states expanded Medicaid and which states didn’t.

{The marketplace} sends you to Medicaid when you don’t meet the minimal revenue requirement. The brand new 2025 Trump tax legislation added necessities to Medicaid for reporting work and neighborhood engagement. You don’t wish to have your revenue fall beneath 100% or 138% of FPL and be topic to these new necessities in Medicaid.

For those who see your revenue is liable to falling beneath 100% or 138% FPL, convert some cash out of your Conventional 401k or Conventional IRA to Roth. That’ll increase your revenue above the minimal revenue requirement.

Say No To Administration Charges

In case you are paying an advisor a share of your belongings, you might be paying 5-10x an excessive amount of. Learn to discover an unbiased advisor, pay for recommendation, and solely the recommendation.